Frequently, when political and economic analysts talk about the Spanish economy on different media, they tend to describe it as “unproductive”, “with high structural unemployment”, or as a model with an “inefficient allocation of resources”. I don’t agree with some of these statements based on historical and empirical references, but that’s a theme for future discussion. Even though I have made reference to it on previous articles and on several chapters of my book In Defense of Freedom , I still think it is important to explain what certain policies should be implemented by the Government to advance towards this dreamed model.

First of all, and in relation to the paragraph above, I think the US would be a good example for Spain to imitate. Why? Well, with exception of some of its protectionist policies, the Trump Administration shows to be registering a huge success in economic terms, and it is no pure coincidence that the first year out of the last 13 when growth goes over the barrier of 3% is also the year with the highest positive variation in capital investment. In this sense, the US has also recently registered one of the lowest unemployment rates in its history, with just 3.9% of the population resting without a job, which is even below the natural unemployment rate!

Sadly, this is not Spain’s case, a country with tremendously high structural unemployment due to its excessively regulated labour market and its overarching bureaucracy. In Spain we have always tried to solve everything with greater public expenditure in the form of investment infrastructure or subsidies to various unproductive sectors. We just need to remember the Plan E and its 7,800 euros in subsidies, which were co-financed by the ICO, with a default rate of 84%. This huge Welfare State has caused the nation’s economy to move in slow motion when going up and to do fast-forward when going down. Slow economic growth during many years and overwhelming debt levels of more than 100%/GDP in many cases have led to the impossibility for millions of young people of finding a job, leading them to question the value of effort and deincentivizing our youth completely.

To prevent sounding dogmatic, I’ll base my opinion on a very important piece of theory. This theory is the Auerbach-Godorilenko model, used to base the effectiveness of expansionary fiscal policies in several situations. The Auerbach-Godorilenko model establishes different scenarios to analyse the effect of these policies: firstly, the cyclic phase of the economy (boom or recession), debt levels in the economy (if debt is over 60%/GDP it’s considered as excessive debt in the model) and finally, the situation of the national financial sector.

The effectiveness of a fiscal policy its calculated by its marginal propensity, so for example if the marginal propensity is 0.6, it means that each new euro of public expenditure employed, will just generate 60 cents of extra growth of GDP. On the contrary, if the marginal propensity is over 1, as for example 1.2, this means that for each extra euro invested in the economy, this will mean that 1.2 euros of extra GDP are create, a consequent gain of 20%. Well, knowing what the concept means, let’s analyse the different plausible scenarios. The Auerbach-Godorilenko theorem establishes that expansionary fiscal policies are just effective in terms of marginal propensity (over 1), when we are in an economic crisis, whit low debt levels (below 60%/GDP) and a correct functioning of the banking sector.

If we introduce Spain in the framework established by this theory, according to several studies published by the two mentioned economists, the marginal propensity of the fiscal expansion will just be 0.8, which earns that by every euro invested by public entities, we will only get 80 cents back. The explanation to this is very simple, as Spain is in a period of economic growth (any positive GDP growth is not considered recession), high public debt to GDP ratio (99%!) and also a situation of stress in the banking system, when the BDE published some days ago that just 2,800 million had been rescued from the 60,000 million bailout by the FROB, with extra 23,000 million by the Fondo de Garantia de Depositos (that was given to the Cajas de Ahorros). So we could consider that the Spanish financial sector is not in a stress-free situation. Well, in this scenario, expansionary fiscal policies are considered to be ineffective, as banks are not looking for greater debt levels, and citizens neither, we are in plain economic growth and our debt to GDP ratio is massive, reducing the influence of new injections in the business cycle.

Consequently, the only plausible solution to promote capital accumulation and economic growth in the long term is by slashing both: taxes and public spending. This is the only way to free capital out of the hands of the State and give it back to its legitimate owners, who independently of how they decide to spend it, will definitely make a productive use of it (consumption, saving or direct investment). As I said before, it’s not a mere coincidence that the US is growing at the greatest rate of its most recent history just after having reduced corporate tax from 35% to 21%, and also lowering income tax in all the various available tax brackets, incentivizing saving and a greater canalization of funds towards the real productive economy, and not towards the destructors of wealth, who we all know who they are… Mr. State & Co.

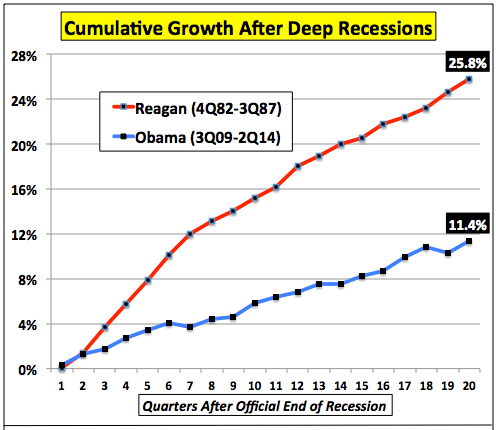

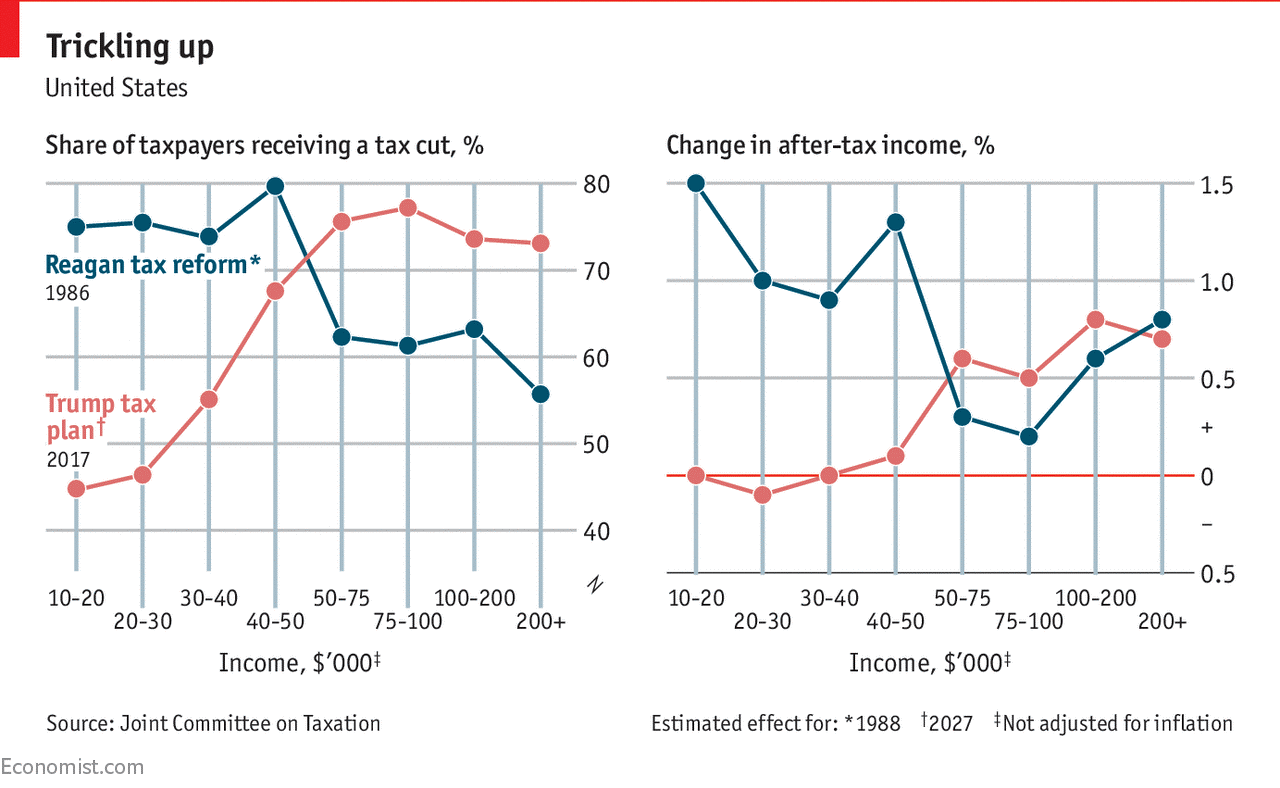

This is not the only successful example of tax cuts, as during the Reagan Administration, in the US in 1984, the highest tax bracket applicable income tax was cut from 37% down to 28%, causing an increase in Capex index and also a great economic growth of 7%.

To conclude, economic growth and socioeconomic development have shown to be two factors boosted by an efficient fiscal policy and a sound monetary system. Liberty and prosperity will prevail.

Estudiante de economía internacional. Defensor del libre mercado desde que tengo uso de razón. Una sola frase para cambiar el mundo: «Laissez faire». Autor de «IN DEFENSE OF FREEDOM», prologado por Daniel Lacalle.

Deja una respuesta